FRTB under Basel IV Series - Article 1 - A confused and staggered Global Timeline

FRTB (Fundamental Review of the Trading Book) under Basel IV* - New required Market Risk cap

New Boundary between Trading Book and Banking Book

This is the fourth in a series of postings by RiskTAE on FRTB under Basel IV.

FRTB has a new specified boundary requirement between the trading book and banking book which will limit the potential for regulatory arbitrage (between the 2 sets of books).

Regulatory arbitrage is a practice whereby firms capitalize on loopholes in regulatory systems in order to circumvent unfavourable regulation. For example, take an illiquid asset out of the Trading Book (hard to mark to market because it’s difficult to do a valuation) and move it to Banking Book (using historic costs). This can result in a lower capital charge. In other instances, banks could move assets between banking book and trading book to reduce the capital charge.

FRTB imposes stringent rules for internal transfers between the trading book and banking book. This includes defining a new boundary based on a bank’s intent:

FRTB states a presumptive list of assets that should be placed in the trading book (i.e., trading book-eligible assets with focus on trading intent) unless there is a justifiable reason exists not to do so.

And, certain instruments will have to be assigned to the banking book, including, for example, instruments being warehoused for securitization.

As noted, the objective of this provision of FRTB is to limit an institution’s ability to move illiquid assets from its trading book to its banking book and, thereby, potentially avoiding higher capital charges if in trading book.

There are further restrictions under FRTB to prevent abuse include requirement for senior management sign off of any regulatory arbitrage through redesignation of assets between the trading and banking book. Such redesignation of assets will require regulatory approval and publication in Pillar 3 reporting. Any capital benefit from this redesignation will be penalised until the position finally matures.

FRTB’s new Trading Book / Banking Book boundary and its very limited permeability in terms of internal risk transfers may put entire trading strategies and business lines at risk due to higher capital costs and increased cost of external hedging with the new FRTB rules for internal transfers.

However, it is not that clear how effective the revised boundary will be in reducing such positioning in all jurisdictions because national regulators are given discretion in defining asset lists.

Banks will need to act fairly promptly to ensure that they carry out a comprehensive review of their Trading and Banking Book positions assignments to meet the FRTB requirements.

Conclusion

Basel IV and FRTB is the most wide-raging comprehensive reformation package especially in the context of data management challenges in the history of the Basel regulations and all-encompassing preparatory work will be required for all areas of the financial institution.

----------

RiskTAE would be glad to discuss your requirements as we have a team of seasoned Risk professionals to deliver solutions.

Do you require any further training, consultancy, or recruitment on FRTB and Basel IV?

RiskTAE can provide on-site training on premise anywhere in the world and can cover many topics across Risk, Governance and Compliance.

Course outlines are available by emailing: education@risktae.com

For all other enquiries, including consulting and recruitment, please email us at: info@risktae.com

----------

RiskTAE has also partnered with an international banking education firm that can provide Basel IV and FRTB Online Self Study courses.

Course outlines for the Self-Study courses are also available by emailing: info@risksexplained.com

Or, you can go directly to the web site: www.risksexplained.com

* - Basel IV is now part of the regular vernacular. Basel IV is not a single regulatory framework, but rather a collection of changing international banking standards. In fact, the Basel Committee views these reforms as simply completing the Basel III Accord and contests the use of the unapproved term ‘Basel IV’. The Basel Committee itself calls them simply "finalised reforms" and the UK Government has called them "Basel 3.1". Critics of the reform, in particular those from the banking industry, argue that Basel IV will most likely require a significant increase in capital and should be treated as a distinct round of reforms being introduced by the Bank for International Settlements (BIS) and its Basel Committee on Banking Supervision (BCBS).

By: Benn Pople (Managing Director, Talent, RiskTAE Limited) and Mark Dougherty (Managing Director, Advisory and Education, RiskTAE Limited)

London, UK – 17 February 2023

Reference: 4 - FRTB Article/Post # 4 - RiskTAE - Topic - FRTB – Boundary

#riskmanagement #frtb #baselIV #basel4 #marketrisk #bankingindustry

FRTB (Fundamental Review of the Trading Book) under Basel IV* - New required Market Risk cap

FRTB (Fundamental Review of the Trading Book) under Basel IV* - New required Market Risk capital cal

What are the Goals of FRTB? This is the third in a series of postings by RiskTAE on FRTB un

“Basel IV” * is one of the hottest topics in global banking. Basel IV is known by many

What Happens to Value-at-Risk (VaR) under FRTB? This is the fifth in a series of postings by

If you still call it “Basel IV*” … you're probably already in trouble. And if yo

We have a deployable Excel-based solution built to help you. The Fundamental Review of the Trading

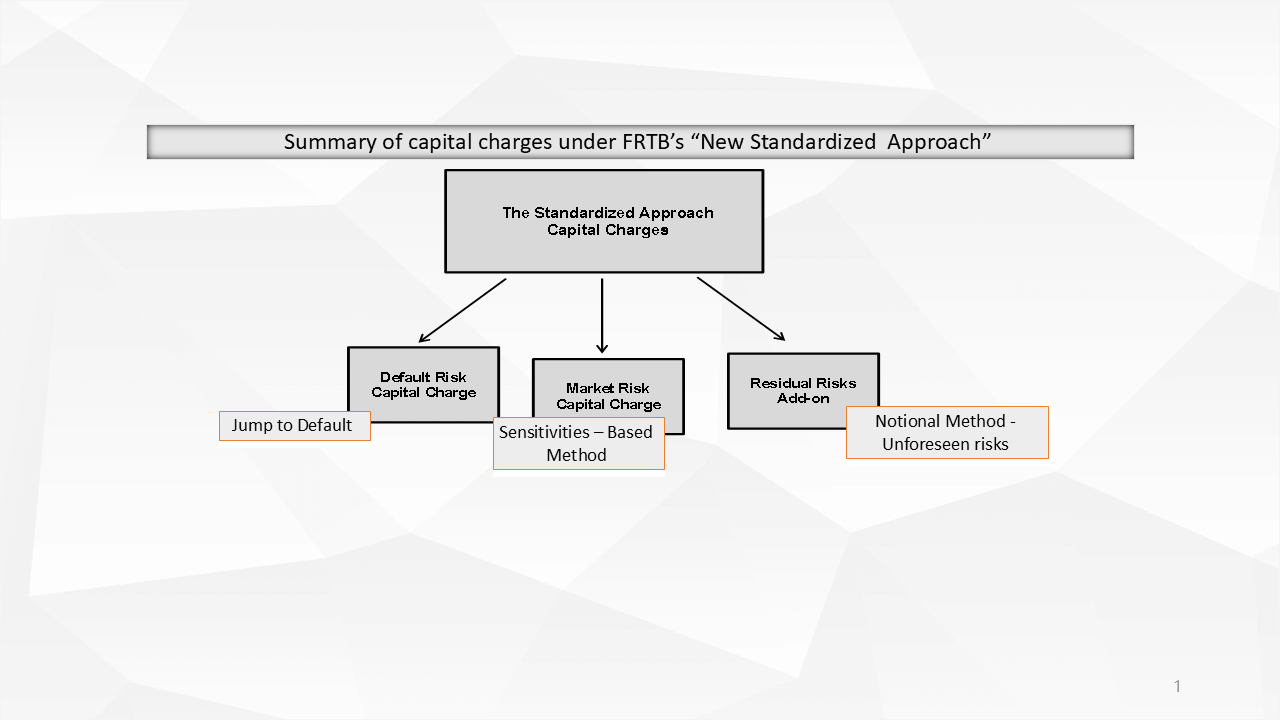

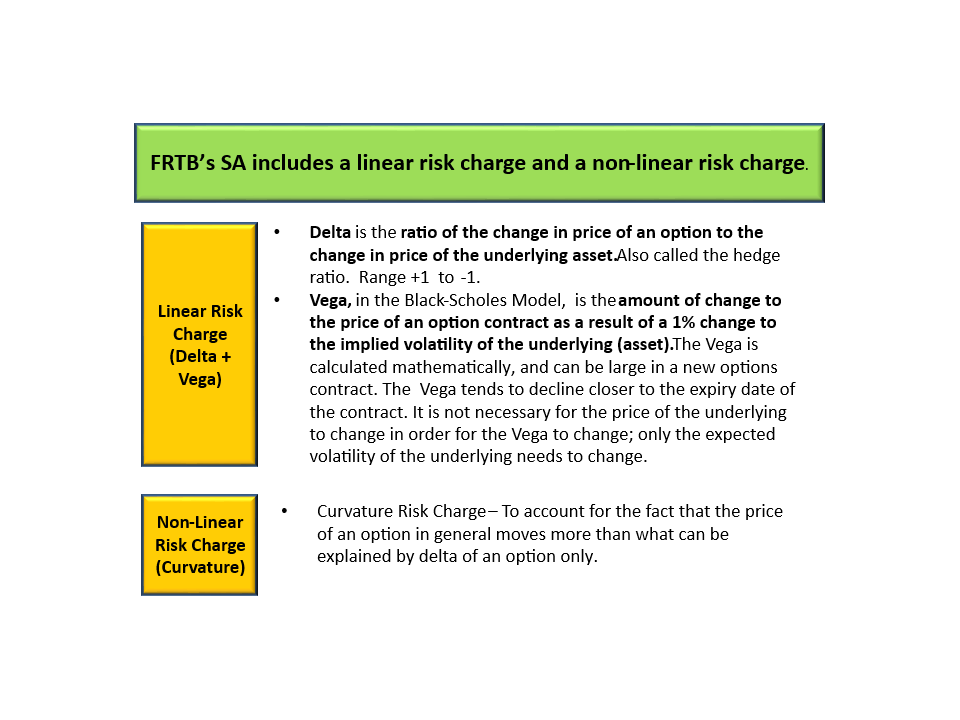

Our Excel model gives you the answer. Under FRTB*, the new Standardised Approach (SA) for capital c

We kept seeing the same thing again and again: Spreadsheets stitched together with fragile logic,

The feedback on our ready-to-use ICAAP, ILAAP and RRP Excel models has been incredible. We are grate

Why has no one offered off-the-shelf models until now? We decided to end the inefficiency. No needl

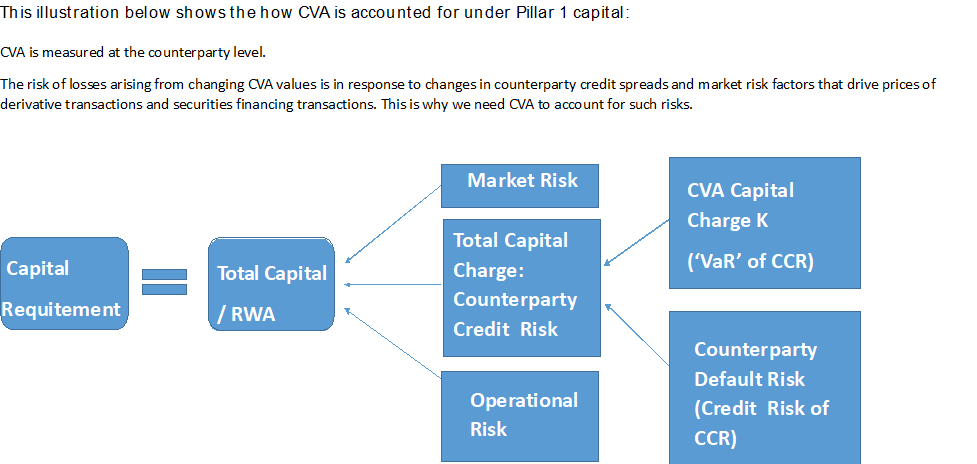

The initial Basel III reforms in 2010 introduced a capital charge for Credit Valuation Adjustment (C

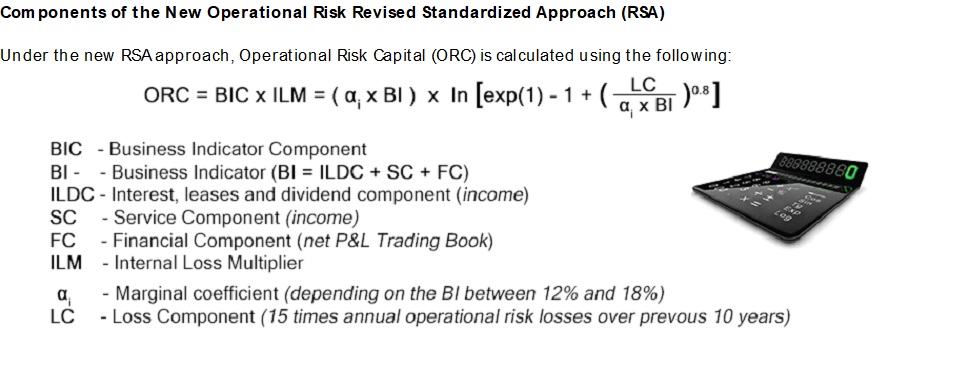

Under the current Basel-related regime (introduced in Basel II), to calculate the minimum capital re

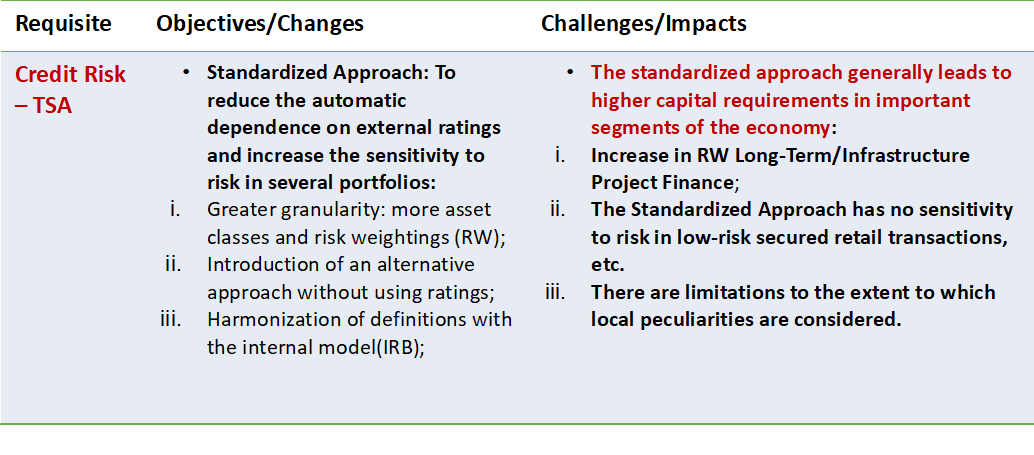

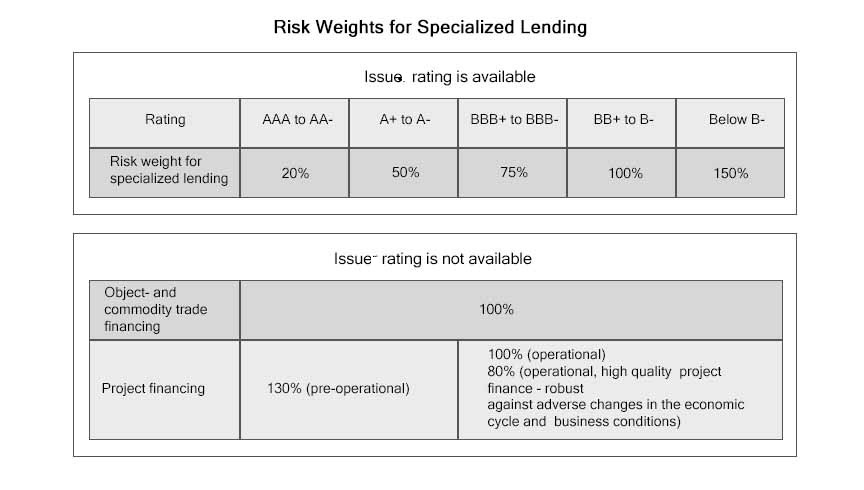

Yet few have a clear view of their delta. If you had to call it today, what’s your delta&hel

Under Basel 3.1/Basel IV/CRR III & CRD VI/B3E, the Basel Committee on Banking Supervision (BCBS)

Under Basel 3.1/Basel IV/CRR III & CRD VI/B3E, the Basel Committee on Banking Supervision (BCBS)

Under Basel 3.1/Basel IV/CRR III & CRD VI/B3E, Basel III Finalised Reforms, etc., the Basel Comm

Due: 31 March 2026 - non-SDDT - We can complete your calculations for you - Data Collection Exercise