FRTB under Basel IV Series - Article 1 - A confused and staggered Global Timeline

FRTB (Fundamental Review of the Trading Book) under Basel IV* - New required Market Risk cap

What Happens to Value-at-Risk (VaR) under FRTB?

This is the fifth in a series of postings by RiskTAE on FRTB under Basel IV.

Background

Basel I (1996 Amendment) regulations required banks to calculate market risk capital based on a VaR for a 10-day horizon with a 99% confidence interval. This provided banks with a current VaR due to the 10-day horizon reflecting a historic period of one to four years.

In response to market risk framework weaknesses exposed during the Global Financial Crisis in 2007, the Basel Committee on Banking Supervision released Basel 2.5, in July 2009. Basel 2.5 added further requirements in the use of a stressed VaR measure to the current value captured by the 10-day VaR but with the stressed VaR using a 250-day period. The intention of the stressed VaR was to measure the behaviour during the longer 250-day period of stressed market conditions. A "stress period" refers to a specific time period during where extreme and adverse market conditions are simulated to assess the potential impact on a bank's trading book portfolio. During the stress period, the market conditions are deliberately set to be significantly different from normal market conditions. This is done to evaluate how a bank's trading book portfolio would perform under severe stress scenarios, which could include sharp market declines, high volatility, liquidity disruptions, or other extreme events.

The goal of using stress periods in the Stressed VaR calculation is to capture tail risks or extreme events that may not be adequately reflected in the regular VaR calculation. By subjecting the trading book to stress scenarios, banks aim to identify vulnerabilities and ensure that they have sufficient capital buffers to withstand severe market shocks.

The Basel 2.5 reforms to market risk were designed to increase capital assessment for trading book activities but were recognised as a stop-gap approach and led to the development of a more fundamental review of the trading book with the first FRTB proposals being released for consultation in May 2012 and finalised in January 2016.

Fundamental Review of the Trading Book (FRTB)

FRTB has introduced a Revised New Internal Models Approach (IMA) for market risk capital (In addition, under IMA, only trading desk-level based is permitted, not for the entire trading floor – this is based on new Desk-level Internal Model eligibility criteria (FTRB moves us from a legal entity authorisation approach to desk level approval system)).

This move is to the new IMA’s Expected Shortfall (ES) – Tail Risk – approach. The ES is the expected value of all changes in the portfolio value in the tail of the P+L distribution that exceed the VaR – the Tail Risk. The Expected Shortfall (ES) is also known as “Conditional VaR (CVaR).” ES is a one tailed statistic measure that quantifies the average loss beyond a certain confidence level (97.5%), usually focusing on the tail of the distribution of potential extreme losses which are not adequately accounted for by traditional VaR calculations and which only provides a single point estimate of potential losses. ES considers the magnitude of losses beyond the VaR level.

Under FRTB, VaR (Value-at-Risk)/SVaR (Stressed VaR) measures can no longer be used for regulatory capital assessment purposes.

The usage exception is that VaR/SVaR are still to be used in stress testing. Under FRTB, VaR (Value-at-Risk) and SVaR (Stressed VaR) are still calculated with VaR at 97.5% (confidence interval) and 99% (confidence interval) for bank wide and desk level, respectively, based on the same risk factors as used for the ES.

Also, the bank cannot backtest with ES and so must still use VaR for this purpose as well.

Impact and Benefits

Higher Capital Requirements: The revised IMA may lead to higher capital requirements for banks compared to the previous version. This is because the new approach introduces more conservative assumptions, such as wider liquidity horizons and more prudent risk factor correlations. As a result, capital charges may increase for certain trading positions.

More Granular Risk Measurement: The shift to a desk-level approval system allows for more granular risk measurement and capital allocation. Instead of calculating capital at the legal entity level, banks can now calculate capital at the level of individual trading desks. This approach provides a more accurate reflection of specific risk characteristics and profiles for each trading desk and allows for better risk management and allocation of capital resources with higher-risk desks having appropriate capital buffers while lower-risk desks benefit from reduced capital charges.

Enhanced Risk Management: Capturing tail risk more effectively allows banks to better understand the potential for large losses during periods of market stress. Banks may now review their risk mitigation and hedging strategies more thoroughly at the desk level. This can lead to more effective risk mitigation practices and the alignment of strategies with the risk profile of each desk.

Alignment with Risk Profile: The revised IMA aims to ensure that risk models are aligned with a bank's actual risk profile. The approach incorporates various risk factors and correlation assumptions that better capture the risk characteristics of the trading book portfolio.

Strengthened Capital Adequacy: The ES approach better reflects the potential capital needed to cover tail risk exposures. This enhances the resilience of banks during adverse market scenarios.

Challenges

Implementing the ES - Tail Risk - approach comes with challenges such as costs to implement significant changes in systems, processes, governance, data quality, model validation, and computational complexity. Accurately estimating ES requires robust historical data, accurate risk factor correlations, and sophisticated modelling techniques.

Conclusion

In the history of Basel regulations, Basel IV and FRTB is the most wide-raging comprehensive reformation package especially in the context of data management challenges and all-encompassing preparatory work that will be required for all areas of the financial institution.

The benefits in the shift to a desk-level Internal Model eligibility criteria under FRTB will impact to market risk capital by enabling more accurate risk measurement, customised capital allocation, improved risk modelling, enhanced data quality, and more effective risk management at the trading desk level.

RiskTAE would be glad to discuss your requirements as we have a team of seasoned Risk professionals to deliver solutions.

----------

Do you require any further training, consultancy, or recruitment on FRTB and Basel IV?

RiskTAE can provide on-site training on premise anywhere in the world and can cover many topics across Risk, Governance and Compliance.

Course outlines are available by emailing: education@risktae.com

For all other enquiries, including consulting and recruitment, please email us at: info@risktae.com

RiskTAE has also partnered with an international banking education firm that can provide Basel IV and FRTB Online Self Study courses.

Course outlines for the Self-Study courses are also available by emailing: info@risksexplained.com

Or, you can go directly to the web site: www.risksexplained.com

----------

* - Basel IV is now part of the regular vernacular. Basel IV is not a single regulatory framework, but rather a collection of changing international banking standards. In fact, the Basel Committee views these reforms as simply completing the Basel III Accord and contests the use of the unapproved term ‘Basel IV’. The Basel Committee itself calls them simply "finalised reforms" and the UK Government has called them "Basel 3.1". Critics of the reform, in particular those from the banking industry, argue that Basel IV will most likely require a significant increase in capital and should be treated as a distinct round of reforms being introduced by the Bank for International Settlements (BIS) and its Basel Committee on Banking Supervision (BCBS).

By: Benn Pople (Managing Director, Talent, RiskTAE Limited) and Mark Dougherty (Managing Director, Advisory and Education, RiskTAE Limited)

London, UK – 23 August 2023

Reference: 5 - FRTB Article/Post # 5 - RiskTAE - Topic - FRTB – What Happens to VaR?

#riskmanagement #frtb #baselIV #basel4 #marketrisk #bankingindustry #VaR

FRTB (Fundamental Review of the Trading Book) under Basel IV* - New required Market Risk cap

FRTB (Fundamental Review of the Trading Book) under Basel IV* - New required Market Risk capital cal

What are the Goals of FRTB? This is the third in a series of postings by RiskTAE on FRTB un

“Basel IV” * is one of the hottest topics in global banking. Basel IV is known by many

New Boundary between Trading Book and Banking Book This is the fourth in a series of postings by R

If you still call it “Basel IV*” … you're probably already in trouble. And if yo

We have a deployable Excel-based solution built to help you. The Fundamental Review of the Trading

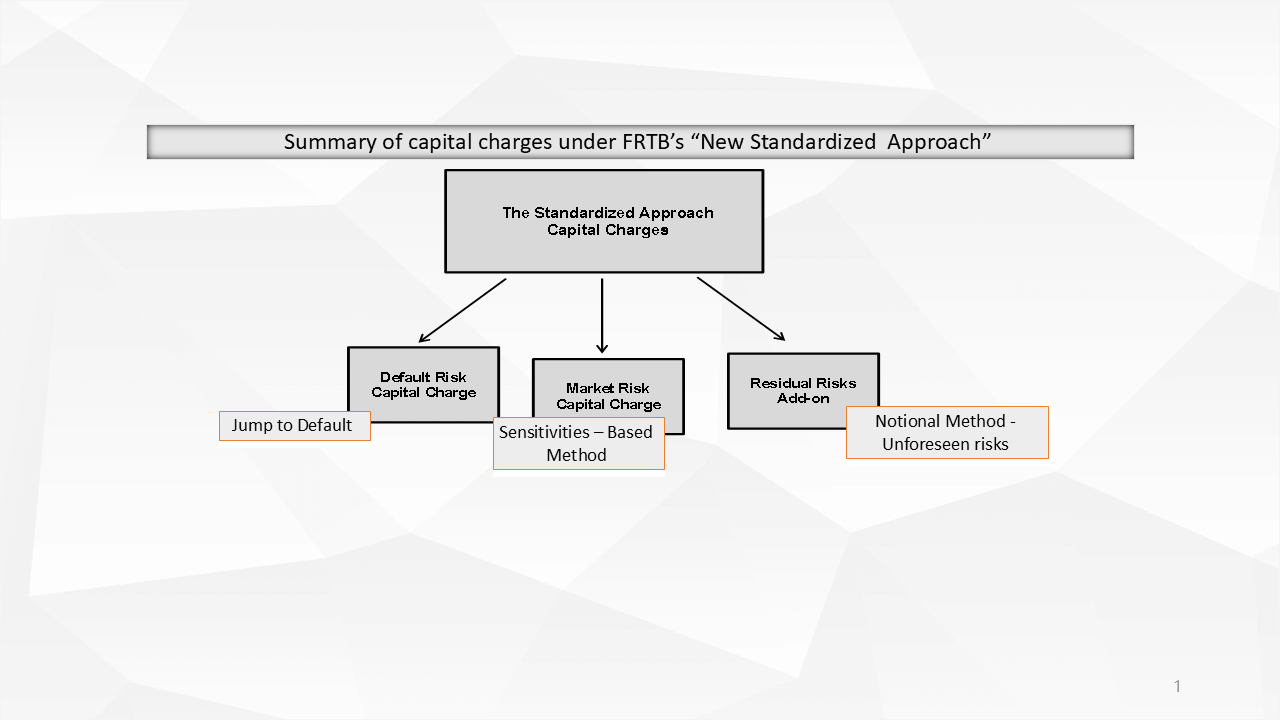

Our Excel model gives you the answer. Under FRTB*, the new Standardised Approach (SA) for capital c

We kept seeing the same thing again and again: Spreadsheets stitched together with fragile logic,

The feedback on our ready-to-use ICAAP, ILAAP and RRP Excel models has been incredible. We are grate

Why has no one offered off-the-shelf models until now? We decided to end the inefficiency. No needl

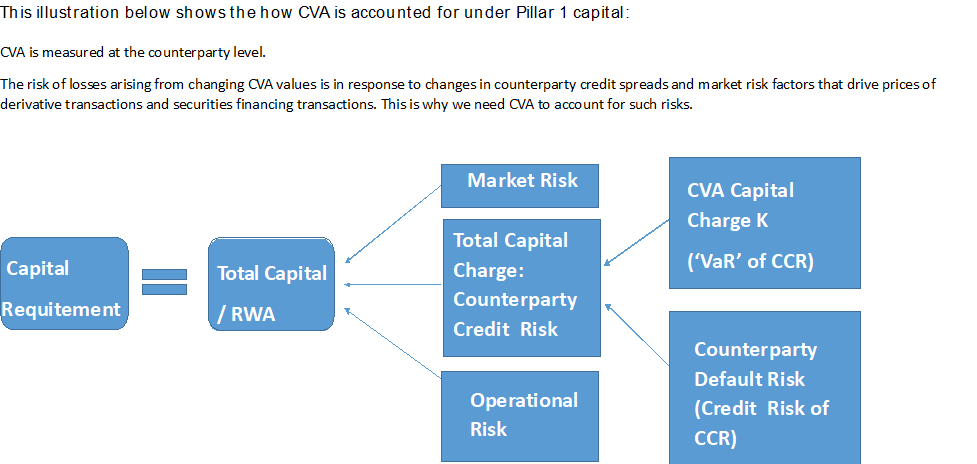

The initial Basel III reforms in 2010 introduced a capital charge for Credit Valuation Adjustment (C

Under the current Basel-related regime (introduced in Basel II), to calculate the minimum capital re

Yet few have a clear view of their delta. If you had to call it today, what’s your delta&hel

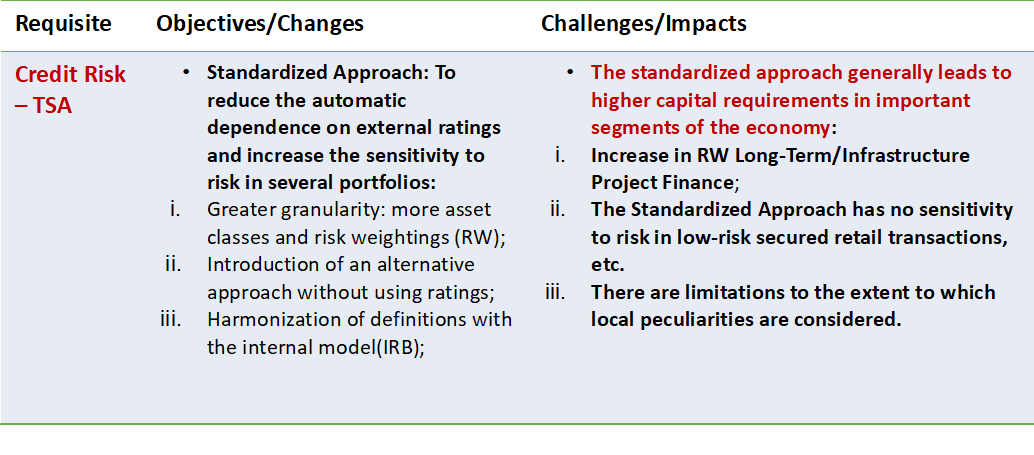

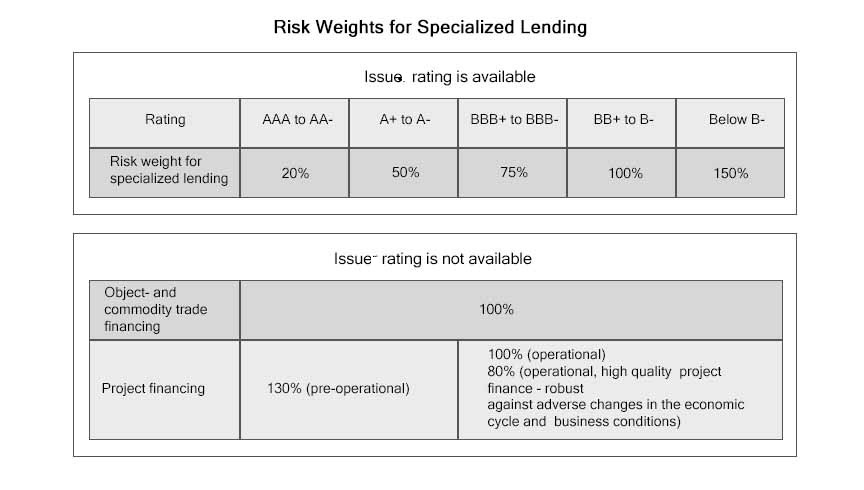

Under Basel 3.1/Basel IV/CRR III & CRD VI/B3E, the Basel Committee on Banking Supervision (BCBS)

Under Basel 3.1/Basel IV/CRR III & CRD VI/B3E, the Basel Committee on Banking Supervision (BCBS)

Under Basel 3.1/Basel IV/CRR III & CRD VI/B3E, Basel III Finalised Reforms, etc., the Basel Comm

Due: 31 March 2026 - non-SDDT - We can complete your calculations for you - Data Collection Exercise