FRTB under Basel IV Series - Article 1 - A confused and staggered Global Timeline

FRTB (Fundamental Review of the Trading Book) under Basel IV* - New required Market Risk cap

Due: 31 March 2026 - non-SDDT - We can complete your calculations for you - Data Collection Exercise - RWA and Other Data - For UK’s PRA Basel 3.1

How to meet the PRA Basel 3.1 RWA and Other Data Submission Deadline – 31 March 2026

Introduction

The UK’s Prudential Regulation Authority (PRA) has initiated a Basel 3.1 data collection exercise, with a submission deadline of 31 March 2026, based on a reference date of 31 December 2025.

This exercise, formally described by the PRA as an off-cycle review of firm-specific Pillar 2 capital requirements, applies to non-SDDT (Small Domestic Deposit Takers), non-exempt firms.

In-scope firms are required to submit a total Basel 3.1 Risk-Weighted Assets (RWA) breakdown, covering:

This is not a routine regulatory return.

The PRA will use the outputs as a key supervisory input to assess how Basel 3.1 affects firms’ RWAs ahead of implementation from 1 January 2027, subject to transitional arrangements.

The PRA’s objective is to use firms’ day-1 Basel 3.1 RWAs to support a potential recalibration of Pillar 2A capital expectations, ensuring that changes in Pillar 1 capital requirements do not result in unintended double counting or mis-aligned capital buffers.

In effect, this exercise provides the PRA with an evidence foundation to rebase Pillar 2 requirements as Basel 3.1 is implemented in the UK.

For CROs and CFOs, this exercise is fundamentally about capital credibility: demonstrating that the firm understands its future risk profile, the capital impact of Basel 3.1, and the robustness of its underlying data and methodologies. For senior management, the exercise is about ensuring that the submission is defensible, coherent and aligned with the firm’s capital narrative.

While the PRA has stated that these data submissions are expected to be on a best-efforts basis, firms should assume the outputs will be reviewed through a supervisory and capital lens, not as a simple dry run. Therefore, firms need to ensure that the data is as accurate as possible.

Background

As part of the second phase of the Near-final Rules (PS9/24), the PRA is undertaking this data collection exercise. This review is designed to support the calibration of pillar 2 to finalise Basel 3.1 in the UK.

The objective of this PRA off-cycle review is to, as part of launching Basel 3.1, to avoid double counting and rebase variable Pillar 2A/PRA buffers as Pillar 1 RWAs change. Or, said another way, the PRA is using Basel 3.1’s day-1 RWAs to reset Pillar 2.

The PRA has set a reference date of 31 December 2025 and a submission deadline of 31 March 2026.

Additionally, the PRA is also collecting data in the areas of “SME lending adjustment” and the “infrastructure lending adjustment”, for the same reason.

Firms eligible for the Small Domestic Deposit Takers (SDDT) regime that have consented to, or notified their intention to adopt, the SDDT Modification by Consent before 31 March 2026 are out of scope for this exercise. Q4 2025)”. The PRA has indicated that a separate similar exercise will follow for SDDTs in Q4 2025.

Submission 1 – Total Basel 3.1 RWAs (Mandatory)

This first template captures the firm’s total risk exposure amount under Basel 3.1, including RWA for:

The authoritative references for the calculations are based on PS17/23 plus PS9/24 except where superseded by CP17/25 (i.e., market risk).

* - PS17/23 – Implementation of the Basel 3.1 standards (near-final part 1)

** - PS9/24 – Implementation of the Basel 3.1 standards (near-final part 2)

*** - CP17/25 – Basel 3.1: Proposed- Adjustments to the market risk framework (subject to finalisation)

This submission is required for non-SDDTs and will form the core supervisory dataset.

Submission 2 – SME and Infrastructure Lending Adjustments (Optional)

This second template applies only where firms wish to evidence eligibility for:

Submission is optional, but for firms intending to rely on these adjustments post‑Basel 3.1, the data will be an important signal of readiness and credibility.

Commercial Reality for CROs and CFOs

From a senior management perspective, this exercise raises three practical questions:

For many firms, Basel 3.1 materially reshapes RWAs across credit, market and operational risk. Treating this exercise as a compliance task rather than a capital planning rehearsal risks surprises later in the implementation timeline

How RiskTAE Can Support Firms

RiskTAE can support banks by delivering independent, regulator‑aligned Basel 3.1 RWA calculations that senior management can rely on for both this submission and capital planning.

Using RiskTAE’s structured data inputs forms and its Basel 3.1‑aligned risk model, we calculate RWAs across all relevant risk classes, including:

The focus is not only calculation accuracy, but explainability and auditability.

What Firms Receive

A Basel 3.1 RWA Calculation Report (Submission 1). Firms will receive a senior Executive‑ready deliverable covering:

This provides a defensible basis for completing the PRA template and supporting Board-level and supervisory discussion.

This service also ensures that you have appropriate processes in place to extract and map data cleanly enough to run the Basel 3.1 calculations.

Optional Support for Submission 2

Where relevant, RiskTAE can also support accurate population of the SME and infrastructure lending adjustment templates, aligned to PRA expectations.

Timing and Next Steps

Although the submission deadline is 31 March 2026, firms that engage early benefit from:

For CROs, CFOs and Senior Management, this exercise is an opportunity to pressure‑test Basel 3.1 readiness before it becomes binding.

For further details or a senior‑level walkthrough, please get in touch.

By: Benn Pople

Email: benn.pople@risktae.com

London, UK

15th January, 2026

FRTB (Fundamental Review of the Trading Book) under Basel IV* - New required Market Risk cap

FRTB (Fundamental Review of the Trading Book) under Basel IV* - New required Market Risk capital cal

What are the Goals of FRTB? This is the third in a series of postings by RiskTAE on FRTB un

“Basel IV” * is one of the hottest topics in global banking. Basel IV is known by many

New Boundary between Trading Book and Banking Book This is the fourth in a series of postings by R

What Happens to Value-at-Risk (VaR) under FRTB? This is the fifth in a series of postings by

If you still call it “Basel IV*” … you're probably already in trouble. And if yo

We have a deployable Excel-based solution built to help you. The Fundamental Review of the Trading

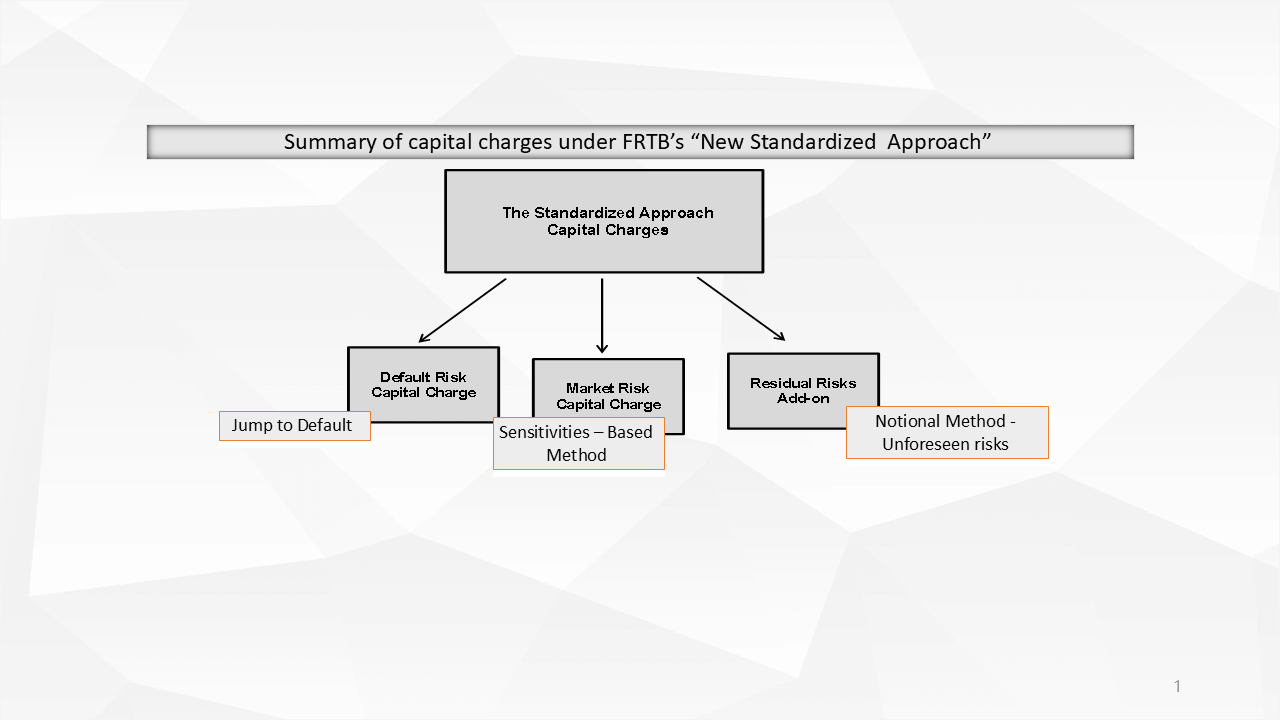

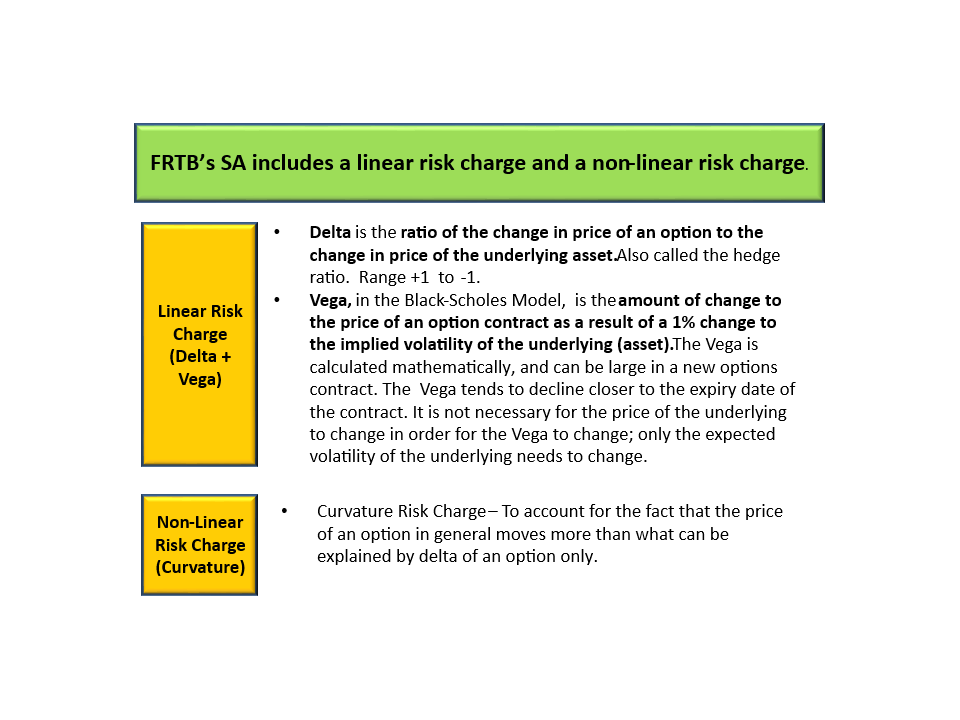

Our Excel model gives you the answer. Under FRTB*, the new Standardised Approach (SA) for capital c

We kept seeing the same thing again and again: Spreadsheets stitched together with fragile logic,

The feedback on our ready-to-use ICAAP, ILAAP and RRP Excel models has been incredible. We are grate

Why has no one offered off-the-shelf models until now? We decided to end the inefficiency. No needl

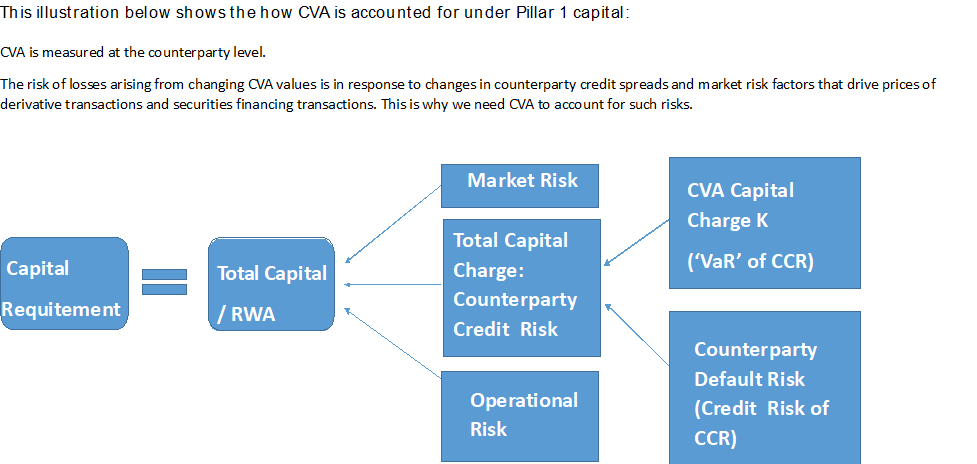

The initial Basel III reforms in 2010 introduced a capital charge for Credit Valuation Adjustment (C

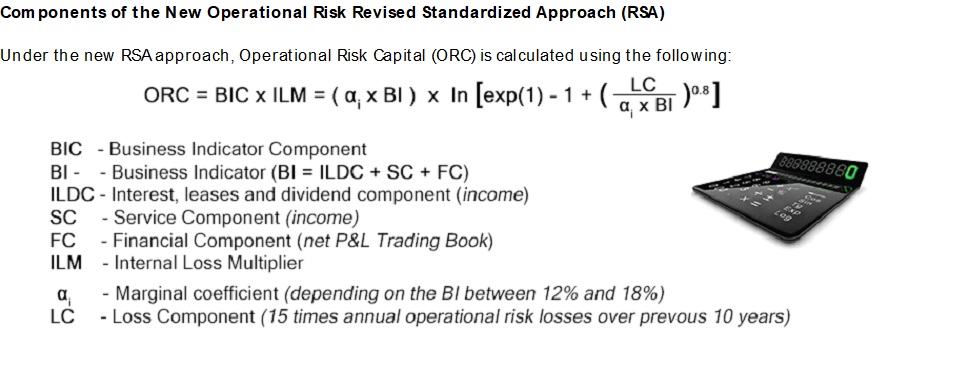

Under the current Basel-related regime (introduced in Basel II), to calculate the minimum capital re

Yet few have a clear view of their delta. If you had to call it today, what’s your delta&hel

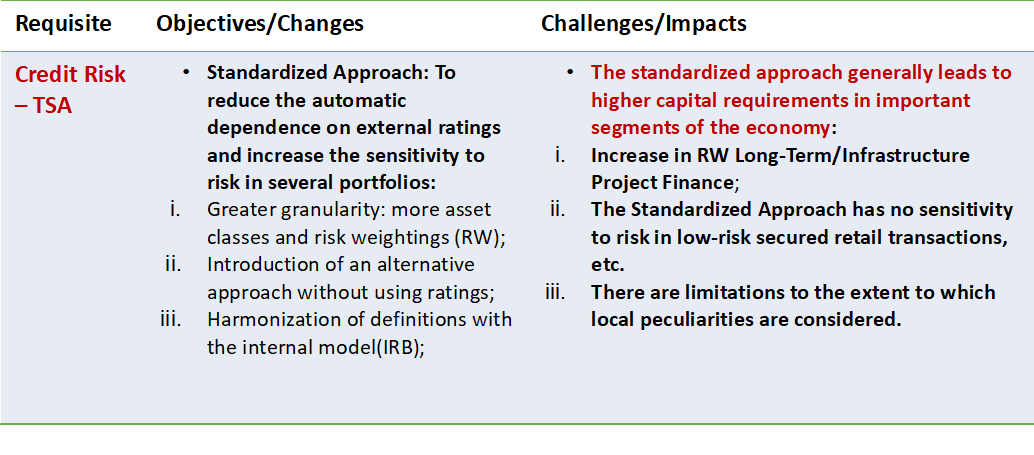

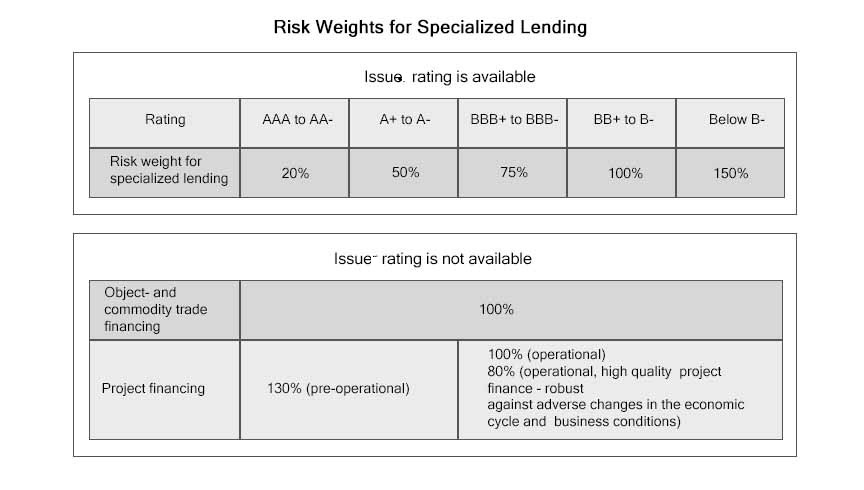

Under Basel 3.1/Basel IV/CRR III & CRD VI/B3E, the Basel Committee on Banking Supervision (BCBS)

Under Basel 3.1/Basel IV/CRR III & CRD VI/B3E, the Basel Committee on Banking Supervision (BCBS)

Under Basel 3.1/Basel IV/CRR III & CRD VI/B3E, Basel III Finalised Reforms, etc., the Basel Comm