FRTB under Basel IV Series - Article 1 - A confused and staggered Global Timeline

FRTB (Fundamental Review of the Trading Book) under Basel IV* - New required Market Risk cap

Under the current Basel-related regime (introduced in Basel II), to calculate the minimum capital requirements associated with operational risk the following approaches are permitted: Basic Indicator Approach (BIA), The Standardized Approach (TSA) & Alternative Standardized Approach (ASA), Advanced Measurement Approach (AMA; an internal model approach).

Under Basel 3.1/Basel IV/CRR III & CRD VI*, the Basel Committee on Banking Supervision (BCBS) introduced the new Revised Standardized Approach (RSA) for calculating the operational risk capital charge, which replaces all operational risk approaches allowed currently under Basel II.

The new Basel IV methodology is mostly commonly called the Revised Standardized Approach (RSA) for Operational Risk. It is also sometimes called the ‘Standardised Measurement Approach (SMA)’.

All firms are required to use this single RSA approach, which factors in historical operational risk losses as well as business indicator measures. No other methodologies are permitted under Basel 3.1/Basel IV/CRR III & CRD VI*.

The revised operational risk capital framework is based on two basic assumptions:

The veracity (accuracy) of these suppositions continues to be debated.

The new RSA for operational risk determines operational risk capital requirements based on the product (i.e., multiplication) of two components:

Therefore, there is positive and increasing (and progressive) synchronicity between the size of a bank and its operational risk capital calculated.

If you wish additional details or a walkthrough, please contact us.

In the next few articles, we'll continue to discuss issues related to the new capital requirements in further detail.

* Basel 3.1/Basel IV/CRR III & CRD VI/B3E/Finalised Basel III.

By: Mark Dougherty, Founder & Managing Director, RiskTAE (Risk Talent, Risk Advisory & Risk Education)

Email: mark.dougherty@risktae.com

FRTB (Fundamental Review of the Trading Book) under Basel IV* - New required Market Risk cap

FRTB (Fundamental Review of the Trading Book) under Basel IV* - New required Market Risk capital cal

What are the Goals of FRTB? This is the third in a series of postings by RiskTAE on FRTB un

“Basel IV” * is one of the hottest topics in global banking. Basel IV is known by many

New Boundary between Trading Book and Banking Book This is the fourth in a series of postings by R

What Happens to Value-at-Risk (VaR) under FRTB? This is the fifth in a series of postings by

If you still call it “Basel IV*” … you're probably already in trouble. And if yo

We have a deployable Excel-based solution built to help you. The Fundamental Review of the Trading

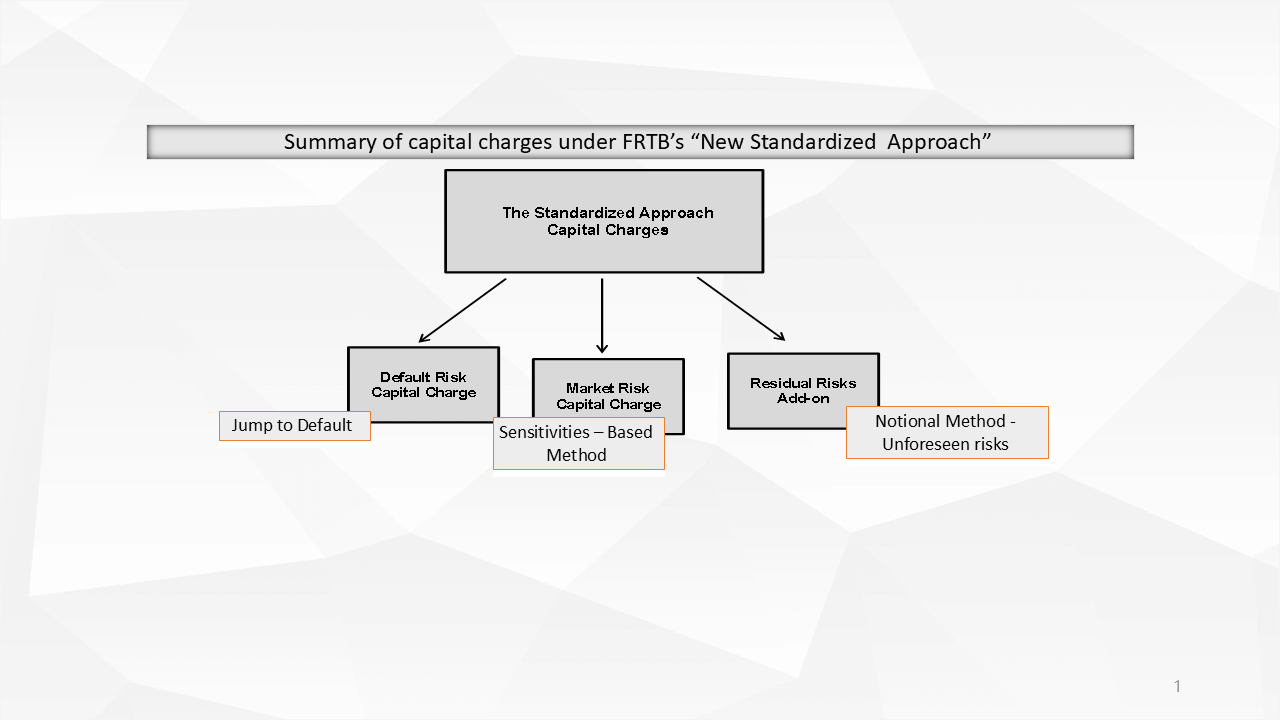

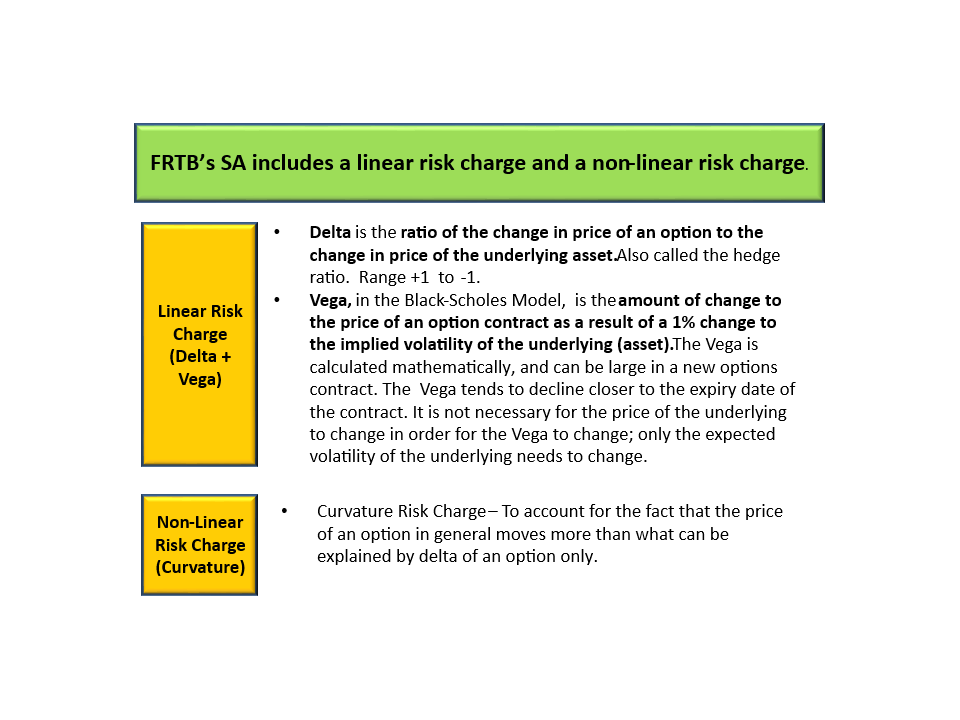

Our Excel model gives you the answer. Under FRTB*, the new Standardised Approach (SA) for capital c

We kept seeing the same thing again and again: Spreadsheets stitched together with fragile logic,

The feedback on our ready-to-use ICAAP, ILAAP and RRP Excel models has been incredible. We are grate

Why has no one offered off-the-shelf models until now? We decided to end the inefficiency. No needl

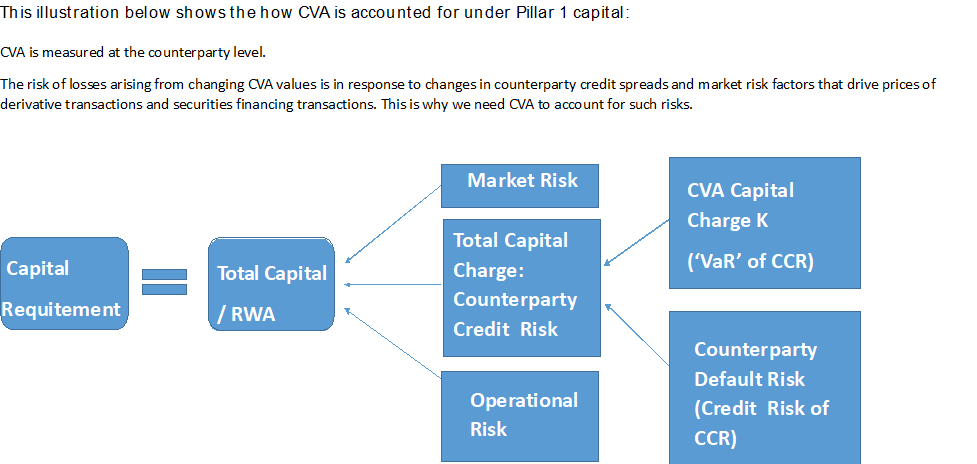

The initial Basel III reforms in 2010 introduced a capital charge for Credit Valuation Adjustment (C

Yet few have a clear view of their delta. If you had to call it today, what’s your delta&hel

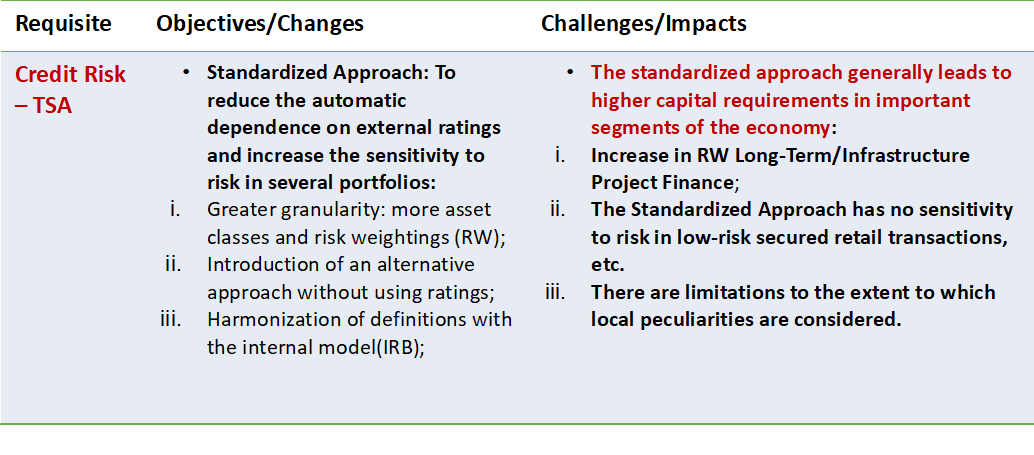

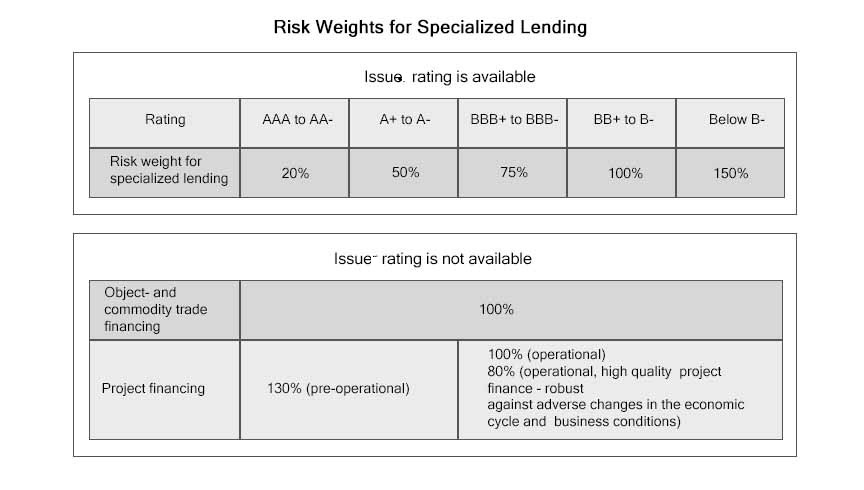

Under Basel 3.1/Basel IV/CRR III & CRD VI/B3E, the Basel Committee on Banking Supervision (BCBS)

Under Basel 3.1/Basel IV/CRR III & CRD VI/B3E, the Basel Committee on Banking Supervision (BCBS)

Under Basel 3.1/Basel IV/CRR III & CRD VI/B3E, Basel III Finalised Reforms, etc., the Basel Comm

Due: 31 March 2026 - non-SDDT - We can complete your calculations for you - Data Collection Exercise