FRTB under Basel IV Series - Article 1 - A confused and staggered Global Timeline

FRTB (Fundamental Review of the Trading Book) under Basel IV* - New required Market Risk cap

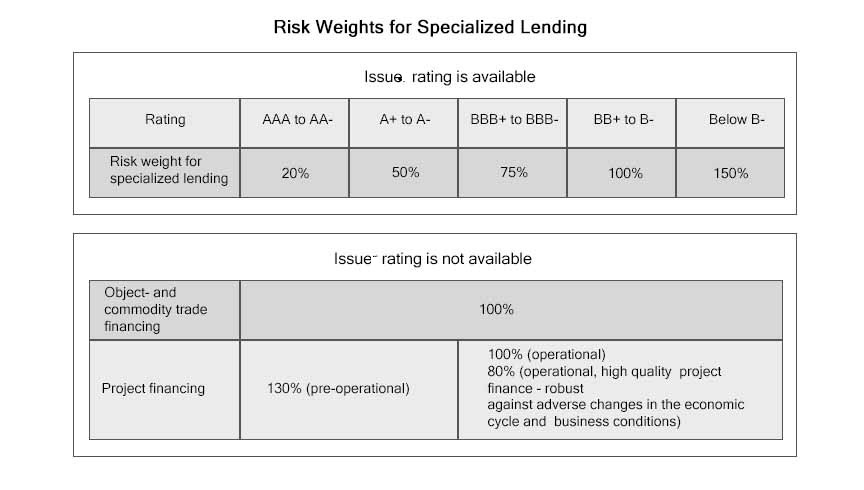

Under Basel 3.1/Basel IV/CRR III & CRD VI/B3E, the Basel Committee on Banking Supervision (BCBS) introduced the new Standardised Approach (SA) calculations for calculating the credit risk capital charge.

Basel 3.1/Basel IV/CRR III & CRD VI/B3E introduces the following changes to the Credit Risk (CR) SA (The Standardised Approach (TSA)) methodology:

RiskTAE has for sale …. Pre and Post

If you wish additional details or a walkthrough, please contact me.

In the next few articles, I’ll continue to discuss issues related to the new capital requirements in further detail.

* The so called “Basel IV*” Accord is known by various different names, including: Basel 3.1 (in the UK), CRR III & CRD VI (in the EU), B3E (Basel III Endgame in the USA), Basel III Finalised Reforms (by the BCBS), etc.

By: Mark Dougherty, Founder & Managing Director, RiskTAE (Risk Talent, Risk Advisory & Risk Education)

Email: mark.dougherty@risktae.com

FRTB (Fundamental Review of the Trading Book) under Basel IV* - New required Market Risk cap

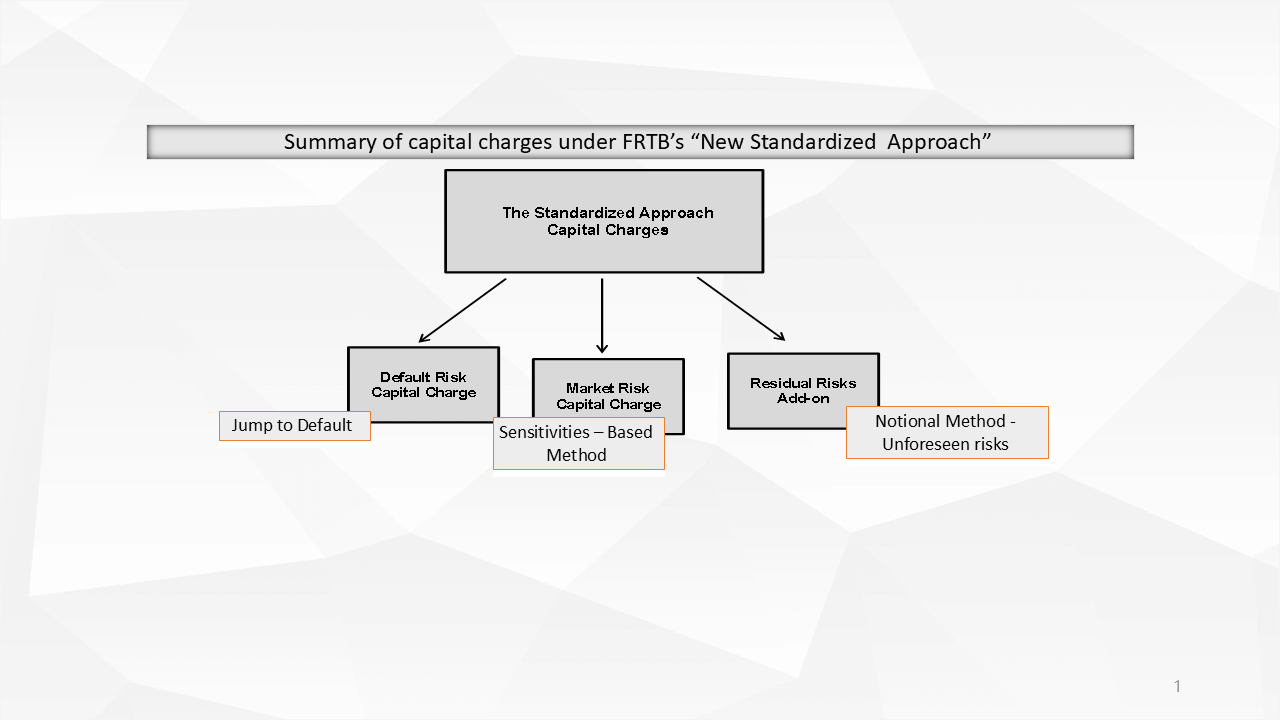

FRTB (Fundamental Review of the Trading Book) under Basel IV* - New required Market Risk capital cal

What are the Goals of FRTB? This is the third in a series of postings by RiskTAE on FRTB un

“Basel IV” * is one of the hottest topics in global banking. Basel IV is known by many

New Boundary between Trading Book and Banking Book This is the fourth in a series of postings by R

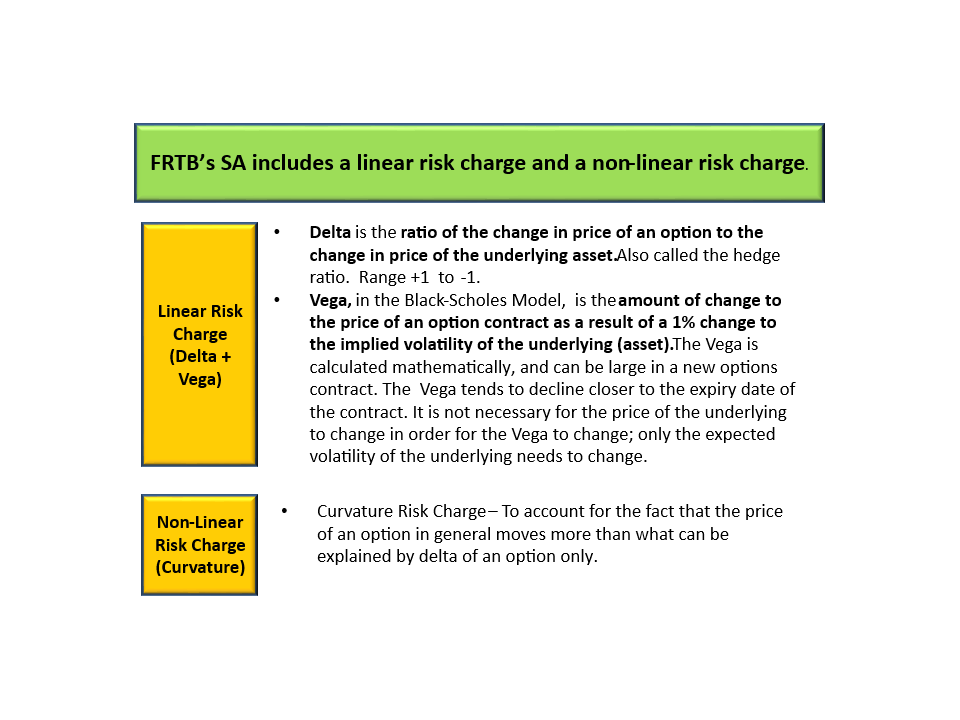

What Happens to Value-at-Risk (VaR) under FRTB? This is the fifth in a series of postings by

If you still call it “Basel IV*” … you're probably already in trouble. And if yo

We have a deployable Excel-based solution built to help you. The Fundamental Review of the Trading

Our Excel model gives you the answer. Under FRTB*, the new Standardised Approach (SA) for capital c

We kept seeing the same thing again and again: Spreadsheets stitched together with fragile logic,

The feedback on our ready-to-use ICAAP, ILAAP and RRP Excel models has been incredible. We are grate

Why has no one offered off-the-shelf models until now? We decided to end the inefficiency. No needl

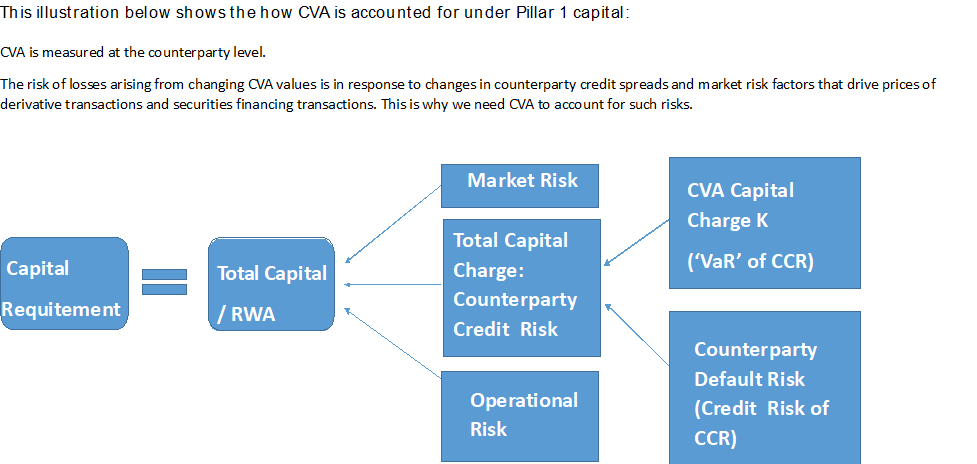

The initial Basel III reforms in 2010 introduced a capital charge for Credit Valuation Adjustment (C

Under the current Basel-related regime (introduced in Basel II), to calculate the minimum capital re

Yet few have a clear view of their delta. If you had to call it today, what’s your delta&hel

Under Basel 3.1/Basel IV/CRR III & CRD VI/B3E, the Basel Committee on Banking Supervision (BCBS)

Under Basel 3.1/Basel IV/CRR III & CRD VI/B3E, Basel III Finalised Reforms, etc., the Basel Comm

Due: 31 March 2026 - non-SDDT - We can complete your calculations for you - Data Collection Exercise